It is important that property owners understand their risk exposure to flood AND are aware that their property insurance policy most likely does not include Flood coverage. There are several options available to your clients for Flood insurance. Here we will discuss ways that your clients can evaluate their risk and determine the right course of action for them.

What is a Flood?

A flood occurs when two or more acres of dry land or two or more properties are inundated by water or mudflow. This is typically the result of an overflowing body of water but could also be oversaturated ground from intense rainstorms causing water to seep through foundation walls, or damage from a hurricane or earthquake storm surge. It is important to note that even if the location has Named Windstorm and/or Earthquake coverage, it will not cover loss from storm surge flooding that results from either of those perils. To be considered a flood loss, the water must come from an external source (not from within the plumbing or sewer system). What many people consider to be a “flooded basement or kitchen” may actually be Sewer & Drain Backup or Water Damage when it comes to insurance.

Read more about the difference between various water-related losses here.

Knowing A Property's Risk

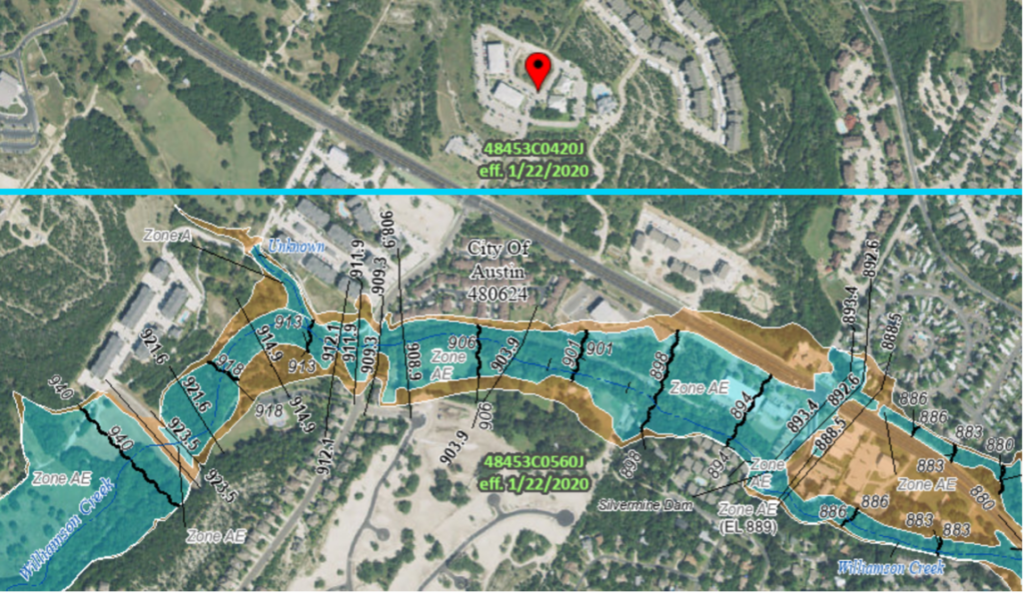

FEMA (Federal Emergency Management Agency) maintains maps of flood zones based on a given area’s risk of flood. These maps identify high-risk flood zones- denoted as letters A (non-coastal) or V (coastal), moderate-risk zones– denoted as letter B or shaded X, low-risk zones– denoted as letters C or X, and letter D zones- areas with possible but undetermined flood hazards. The REInsurePro tech platform pulls the flood zone for you. You can look up a flood zone here.

Most mortgage companies lending on a property in an A or V zone will require that the property owner carry flood insurance. This is common for federally-regulated or government-backed lending institutions.

However, even if the property is not in a high-risk flood zone, the property owner may still be exposed to loss from a flood. In fact, 20-25 percent of flood losses nationwide are outside of a high-risk zone. Even in a moderate-risk zone, there is a higher than 1 in 4 chance it could be flooded during a 30-year mortgage, which is more likely than a fire. The average flood loss can cost nearly $40,000, so flood insurance should be considered for any property, regardless of location.

What Flood Insurance Covers

A typical flood policy will have a set building coverage limit (commonly $250,000) and will cover:

- Essential systems in the home (such as electric and plumbing, furnace, HVAC, etc.)

- Appliances

- Carpet

- Walls and built-in cabinets and shelves

- Foundation walls

- In many cases, a limit for a detached garage.

Usually, personal property coverage can also be purchased up to a defined limit.

What is NOT covered includes damage by mold or mildew from a flood that could have been avoided, additional living expenses or loss of use if the resident has to relocate for a period of time, cars or vehicles, and oftentimes contents that are in the basement.

Exploring Options

There are several options to consider when it comes to Flood Insurance.

NFIP

FEMA administers the National Flood Insurance Program (NFIP), which is backed by a network of over 50 insurers. On October 1, 2021, FEMA launched Risk Rating 2.0, a new pricing methodology in which flood zones are no longer used to calculate rates. FEMA notes, “Under Risk Rating 2.0, premiums are calculated based on specific features of the individual property- including distance from water, type of flooding, flood frequency, structure foundation type, height of the lowest floor relative to Base Flood Elevation (BFE), and the structure’s replacement cost value. Risk Rating 2.0 also adds pluvial flood risk—flooding from heavy rainfall.”

These policies offer up to a $250,000 building coverage limit for residential properties and $500,000 for 5+ units, plus the option of purchasing up to $100,000 of personal property coverage. FEMA’s offering is an annual policy.

NFIP drawback: There is a 30-day waiting period to obtain coverage unless it was purchased when the property was purchased or the area is newly designated as a high-risk flood zone. NFIP is an annual policy that can only be canceled mid-term for a limited number of approved reasons (e.g. the mortgage was paid off, the home was sold, or the location is no longer in a high-risk area after a map change).

Private Flood

Flood Insurance is also available through private insurers. While coverage will be similar to that under the NFIP, private insurers can set their own rates based on a wider variety of factors, especially related to the building itself (age, square footage, number of stories, etc). Private flood options are also typically more flexible with coverage limits, waiting periods, and additional coverage options.

Our Program Flood master policy can be purchased as an add-on to your client’s current coverage. The upsides of this option are that it is included in the monthly schedule and bill, it remains in force unless it is canceled (no annual payment or renewal), AND there is no waiting period– coverage can start right away. Properties with one to four units can obtain up to $250,000 of coverage and five to twenty-unit properties can obtain up to $500,000 of coverage, subject to a $1,000 deductible ($5,000 in Massachusetts).

Although this coverage is equivalent to NFIP, some lenders will only accept NFIP.

It is strongly encouraged to offer your clients flood coverage and be sure that if they decline that coverage, they know their exposure.